The Interest Rate Fallacy and The Myth of the Fed

The Interest Rate Fallacy and The Myth of the Fed

No one understands money, who makes it, or how much it costs.

Most people who are freaked out by inflation right now will point to low interest rates as this bogeyman; the ultimate reason for this insane, worldending sky-high inflation that we’ve seen! These same people also aren’t very familiar with what recency bias is, and how they have a severe case of it.

I would like to dispel a couple of myths that people seem to hold as pillars of truth, these days. The first being the Interest Rate Fallacy, something that Milton Friedman thoroughly described fifty-two years ago, and yet people still seem to think low interest rates mean that money is loose, and that high interest rates mean money is tight. To even understand his fallacy, however, we must understand what “interest rates” even mean and what moves them.

The second will be how the Fed is this omnipresent financial god that “controls rates” and “controls inflation.”

What Are Interest Rates?

US Treasury Rates are the benchmark for all interest rates in our country, as any interest-paying security has to directly compete with it. Why? Because the US Treasury is the undefaultable 100%-guaranteed risk-free debt of not only government, but the United States Federal Government. This is why, as I have described in the past, US Treasuries are the most pristine form of collateral used in the global financial economy. When you are given an interest rate for a loan, your credit and history are taken into account, but the interest rate of a similar maturity Treasury rate is taken into account. If you get a 30-Year Mortgage, your rate is locked in (assuming it is fixed-rate) in accordance with whatever the 30-Year US Treasury is at the time. If a 30Y is yielding 2%, your mortgage will probably be something like 3.5% or so. It is a signal, to the economy, of what kind of yield an investor is able to get from an interest-bearing security. Well, what actuates interest rates?

What the Fed Actually Does Do

You might think, from your consumption of fintwit and cable news that it’s Jerome Powell actuating a secret lever, that only he, after consulting other Fed Presidents, can actuate. When really, it is much more complicated than just a direct actuation of the flow of money in and out of the real economy. In principle, a central bank is supposed to do exactly that. Unfortunately, as we have learned from the Eurodollar System, most of the US dollars in the world’s real economy are uncounted and unreachable by the Federal Reserve (the Fed). Why? Because when central bank reserves are given to banks, and loans are made, once you take money out of a bank, it is totally off the balance sheet of anyone. Paper/Fiat currency is untrackable. That’s what the Pandora Papers really proves - there was trillions of dollars just floating around offshore banks that no one really knew about.

When interest rates are adjusted, what is specifically happening is the Fed is now aiming for a certain federal funds rate that is hopefully achieved. What is the federal funds rate? It is the rate at which banks can borrow and lend to one another. Effectively, it is set by no one, but when the Fed changes its “target” rate, it is changing how much is available for banks to borrow. The weird thing, though, is the Fed Funds Rate doesn’t matter anymore because the (Central Bank) Reserve Requirement is officially 0 and will stay that way for, it seems, the rest of existence. This allows banks to not have to hold any amount of bank reserves.

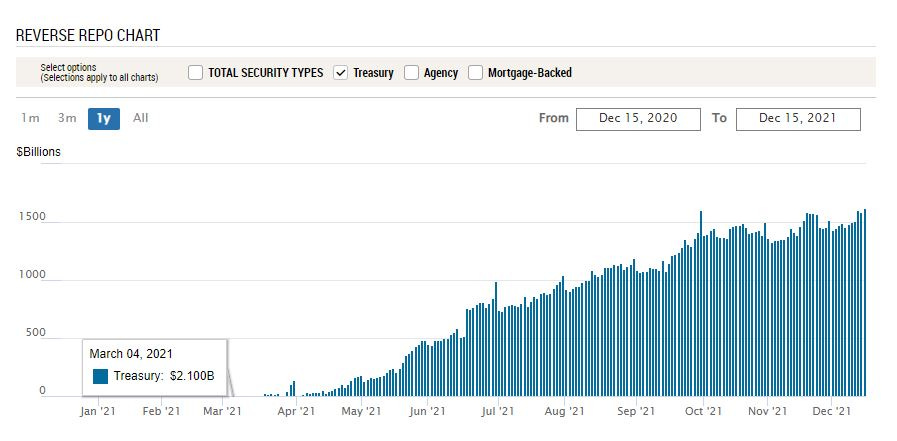

So what does the Fed control? Well, they issue the Treasuries into the market, which provides access to collateral, and primary dealers are legally obliged to hold auctions, so it not only provides a checks and balances, but also makes sure that the Treasuries will always be bought and cannot be no-bid. It is functionally impossible for Treasuries, from T-Bills to Bonds, to default. The Fed also controls the rate of IOER (Interest on Excess Reserves) and the Repo and Reverse Repo Facilities. We have talked about IOER and Repo several times before, but essentially these rates are irrelevant to the interest rates you see in the real economy. IOER just encourages banks to park extra reserves at the Fed (no reason to anymore), Repo is how they can get cash by using their Treasuries as collateral, but the extremely important one is the Reverse Repo, because it is really the only main facility that is being used to an excessive degree. Reverse Repos, which is banks trading their central bank reserves for overnight/very short-term Treasuries, has become extremely popular. On the daily, they have averaged $1.5 Trillion for a couple months, which has gone up from a few billion in March and April. Before March, it was hardly ever used to such a degree.

Why do banks want Treasuries? Well, again, I’ve explained it before, so in short: they need these Treasuries to stay alive in the many transactions and trades they have everyday. It is the pay-to-play collateral that allows them to stay in the game. There is such a lack of trust in the system right now that banks would rather use the majority of their spending capabilities on simply just having Treasuries. Before 2008, they simply created this collateral out of thin air with private-label MBSs. You can imagine why that didn’t last very long, and why the entire banking system is on thin ice.

So the Fed does nothing, really, and what they actually do do isn’t all that inflationary. You might bring up QE, that old chestnut, but I’ve, again, explained that in a previous video which I recommend everyone go watch so they can learn why it literally does nothing and is utterly ineffectual. When you see a headline that says the Fed “adjusted interest rates,” what that means is they adjusted the target interest rate of a transaction in the banking system that doesn’t really matter. So, you might be yelling at the screen right now and saying, “Okay! We get it! The Fed doesn’t do anything! So who changes interest rates!? Why are they so low!?”

Interest Rates Are a Mirror of the Real Economy

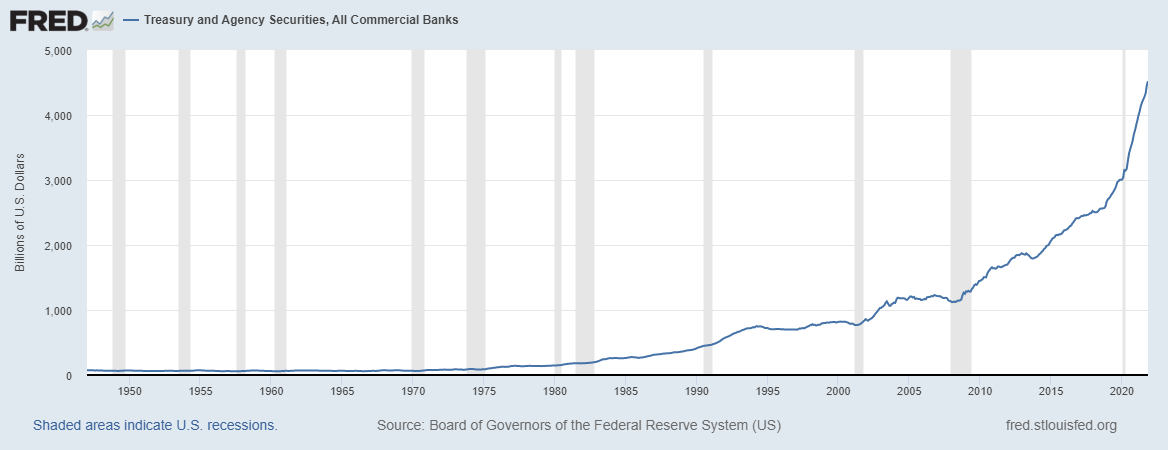

When interest rates are this low, it isn’t a reflection of an out of control central bank! It is a reflection that investors and banks would rather park money in corporate and government bonds, than to loan their money out to ready and willing young bucks itching to start a business. If you don’t agree with me, then please go back and look at the “Treasury and Agency Securities, All Commercial Banks” chart. That is a reflection of heavy buying of Treasuries - AKA Big Money don’t wanna lend to main street, but keep their money in safe assets. Not only because they don’t trust the real economy, but they don’t even trust other damn banks.

To explain how interest rates work, I’ll take from Investopedia because they’re the best:

As bond prices increase, bond yields fall. For example, assume an investor purchases a bond that matures in five years with a 10% annual coupon rate and a face value of $1,000. Each year, the bond pays 10%, or $100, in interest. Its coupon rate is the interest divided by its par value.

If interest rates rise above 10%, the bond's price will fall if the investor decides to sell it. For example, imagine interest rates for similar investments rise to 12.5%. The original bond still only makes a coupon payment of $100, which would be unattractive to investors who can buy bonds that pay $125 now that interest rates are higher.

The higher the interest rate, the more risky a bond is. Why? Because it is cheap, and therefore the interest rate reflects the amount of risk you are assuming.

When interest rates of government bonds are high, it is because the government is issuing so much debt in comparison to how much its debt is in demand, therefore it has to attract buyers by bidding the price down. Well, what are US Treasuries looking like? They’re at all-time lows because there is so much demand for them, not only as risk-free yield, but because they’re the safest bet to put money into when the global economy is slowing down like it is, and when collateral is needed to stay in the game.

Low interest rates means there is high-demand for bonds, AKA tight money, as in money is not ready to be thrown into big investments (think of what it was like in the 1980s with REITs. Money was much looser than it is now.) High interest rates means there is low-demand, and money is more interested in spreading around and risking big. It ties back to money velocity being half of what it was in the late 1990s. Money is not as ready to be spent as it used to be.

So What About Inflation and The All-Time High Stock Market?

The stock market does not reflect the real economy. It never has, it never will. Dumb people gambling what money they do have on stocks has happened before in highs and lows. I will talk about inflation, but one thing people don’t get is that stocks are not, nor have they ever been, inflation hedges. Secular inflation, like we had in the 1970s, are comorbid to terrible stock bear markets. The minute we get real inflation, money will outflow from stocks in a jiff, and go right into the necessities. Likewise, the same happens with deflationary eras, where money will outflow from stocks into Treasuries and long-term, safe assets like dollars, and even gold.

What I would like to ask the typical inflationist, who normally ranges from someone who has little to no knowledge of the dollar funding market, central banking, or the history of secular inflation and deflation events, but they have immense recency bias and see their favorite pundit blabbering about inflation. Then, there are people who have a considerable knowledge about economics, normally are from the Austrian School, and have this belief in the bewildering, magical “business cycles” and how we are going to go through an era of massive secular inflation due to moneyprinting.

Neither seem to understand the basics of central banking, and how the printing of central bank reserves doesn’t cause inflation because of the disconnection from the real economy, or how the amount of dollar-denominated debt across the world will always outmatch whatever money is put into the real economy by the Fed, or how regardless of if the Fed buys Treasuries, they are so in-demand from rehypothication (where the same Treasury is used as collateral by one to three dozen parties) that there’s no way the Fed could count every Treasury in the world to meet the exact demand that is required to somehow push interest rates down even a tad (it would literally take quadrillions of dollars). No, see, these guys are smart, they saw Peter Schiff talk about how gold is number one, or they saw how Raoul Pal is all-in on Bitcoin, and how the dollar is gonna flipping crash because a Democrat said somewhere that they’re gonna forgive college debt! Oooo spooky!

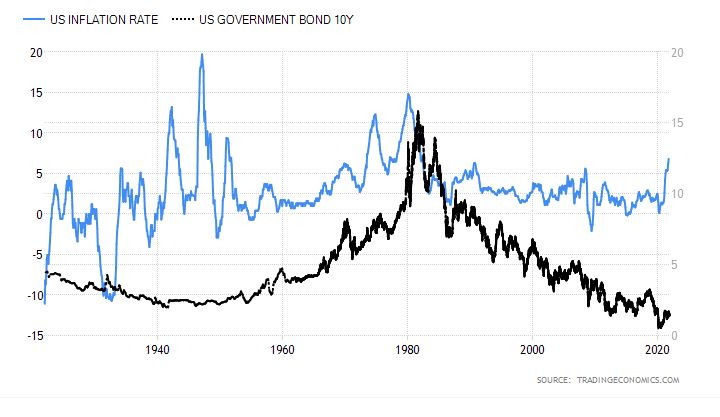

What they never seem to realize is the bond market has predicted inflation in the past, as Big Money sells off treasuries, either in anticipation of inflation, or because they are risk-on, and interest rates subsequently go up. Why is Big Money not doing that now? Because Big Money does not predict inflation.

In the 1950s, when inflation spiked at the onset of the Korean War, interest rates didn’t move a nudge. Why is that? Mr. Big Money didn’t see a reason for this obvious transitory move in inflation to mean anything in the long-term, or even short-term, economy. Instead, he held on. When a secular inflation event started rearing its head in the 1960s, the sell-off began, and as inflation exploded, interest rates exploded. This was not a government spending event, nor the overblown gold window being shut in 1971 - no - it was simple honest dollar proliferation around the world, as well as US nominal growth in GDP, that led to inflation spiking the way it did. Once it was clear inflation was subsiding, interest rates let off.

Hey, even look at now, rates rose ever so slightly from their all-time lows in 2020, but not by much, and have had a hard time getting back over ~1.75%. Every time the 10Y gets close to 1.75%, it falls back out of bed. And yet inflation seems to be sky-high? It is. It just isn’t going to last for 10-15 years like it did in the late 60s to early 80s. Instead, it will last 10-15 months like it did in the early 1950s.

Conclusion

It’s simple really. High interest rates means money is ready to be spent and spent like mad. Normally it is due to economies doing well, or due to secular inflation events from too much money in the real economy. Low interest rates means money is ready to be parked in a safe area and not toyed with until the coast is clear.

The fact Powell rescinded his “transitory” comment is nothing more than optics so he can pretend that the economy still needs a bit of a nudge, when really all of this “tapering” and “selling assets back into the market” is a drop in the bucket to where rates are going (back down) and where inflation is going (back down).

In two years, when the economy is still in the crapper, rates are near all-time lows, inflation is back under 2%, people’s jobs are still shit and paying them squat, and tension is worse than ever, I want all of you to remember how wrong everyone is and why you need to stop listening to the Fed, stop listening to the news, stop listening to these alarmist inflationists who pretend they know everything and that if you just buy their pet asset, you’ll be okay.

We aren’t headed anywhere except down. Everything is pretty much pinned on the financial economy holding itself together, and the timing of its breakage, as well as a cornucopia of other things geopolitical and geoeconomic.

“The nature of the game as it is played is such that the public should realize that the truth cannot be told by the few who know.”

Jesse Lauriston Livermore