The Great Contraction: A Theory on Credit Expansion/Contraction

The Great Contraction: A Theory on Credit Expansion/Contraction

Why economies boom and bust

The long-drawn out era of low growth that came after 2008, that we are still in, is not an especially unique phenomenon. Now, the issue with MBSs and ABSs, and the little intricate cogs of the banking system snapping and breaking is definitely special, but the broad idea of extended economic contractions is nothing new.

With this post, I would like to pose an important broad explanation that will help us understand what brings about expansions that inevitably end in contractions, and how we are encountering an epoch of contraction.

Let us start with an example we all know quite well:

October 28, 1929

Black Monday was a harrowing day that would live in infamy for many years to come as the excess debt that had been created by a previous credit expansion finally came to a head. Much like draining a pimple so that it will finally go away, the system had been experiencing a massive “what’s next” problem. This problem, in specific, is what I see as the final end to a credit expansion, and the beginning of a credit contraction.

What led to this massive run up in the stock market, issuance of debt, and general market mayhem? Technology and population. Around the 1880s and 1890s, it became quite clear the Western World was facing a new era of scientific discovery. We had invented ways of recording sound, and then sight. We had constructed our first engines that would run our first vehicles that could make a several day journey into a single day one. Not only that, we now could go to the restroom that was connected to an elaborate sewage system, and on our way to that restroom, we wouldn’t have to light a dim candle, but snap on an electric light to make that journey much more convenient and safe.

All of these massive discoveries and inventions became marketable consumer good within a generation, and by the 1920s, everyone could afford a Ford Machine and an Edison Electric Lightbulb. Where someone’s grandparents lived off the land in near-medieval lifestyles, young people had only known this brave new world of grand technology.

But with great expansions, comes a great question after all these inventions have been made, and along the way, debt has been crafted to an extreme extent in the background.

Some of y’all might know Duesenberg Motors Company. The German brothers who started the company were just as innovative and idealistic as Henry ford. They came to America to live the American dream and start a company whose focus was utterly dedicated to crafting the most luxurious transportation machines you’d ever laid your eyes on. If you were driving a Duesenberg, you weren’t just rich - you were special. However, Duesenberg, and many like them, faced an issue when debt issuance became less loose in the 1930s. They couldn’t get the liquidity to maintain their very niche industry, and all the people who would want a Duesenberg, and could afford it, were either bankrupt or trying to maintain what little they still had. That’s why by 1937, Duesenberg was defunct.

It wasn’t that they were a bad company, and had bad products, but they were simple excess.

Why couldn’t debt keep being issued, though? Yanno, to keep good guys like the Duesenbergs in business. Well, that’s the ultimate issue - when there is too much debt, and not enough expansion to keep that debt rolling over, the system will collapse at some point as it tries to drain excess debt/credit that it cannot maintain.

So based on this interesting era from the 1880s to the 1930s, it began with humble beginnings, risky men willing to make big bets, credit expanded as the financial industry wanted to make big money on the potential for these big ideas to make big money, bad and unrealistic bets were inevitably made as these eras of loose money meant there ends up being some “misallocation”, and the system ends up collapsing as the bad bets become too numerous, and the regime of technological expansion comes to an end. If you cannot maintain debt, it must be drained.

This also leads to inflation, which is where many of my Austrian friends may take issue. Inflation is a good thing because it is the process of excess demand in an economy. That means there isn’t enough stuff, but there is all this organic wealth being created. This inevitably leads to credit expansion and creation of jobs, stuff, and opportunity. In credit contractions, like we are living in now, there is little organic wealth being created, therefore jobs and opportunities are not as easy to get, and stuff is not as easily financeable. (This should be plainly obvious by the amount of crap you have to do to get a job your grandpa could’ve gotten by just walking up and asking.) Likewise, money is no longer loose, because credit is not expansionary which is why we had dismal inflation throughout the 2010s as apposed to the mid-1980s to the mid-2000s. This doesn’t mean inflation can’t be sustained by moneyprinting - it obviously is created by that in other situations, and I am in no way saying that that is a good thing. I am simply providing analysis as to why it happens in credit expansions, and why it is a signal of something beneficial.

Now that we have a good understanding of where these expansions come from, and why they inevitably lead to contractions, we must take this analysis and apply it to the economic regime we now live in:

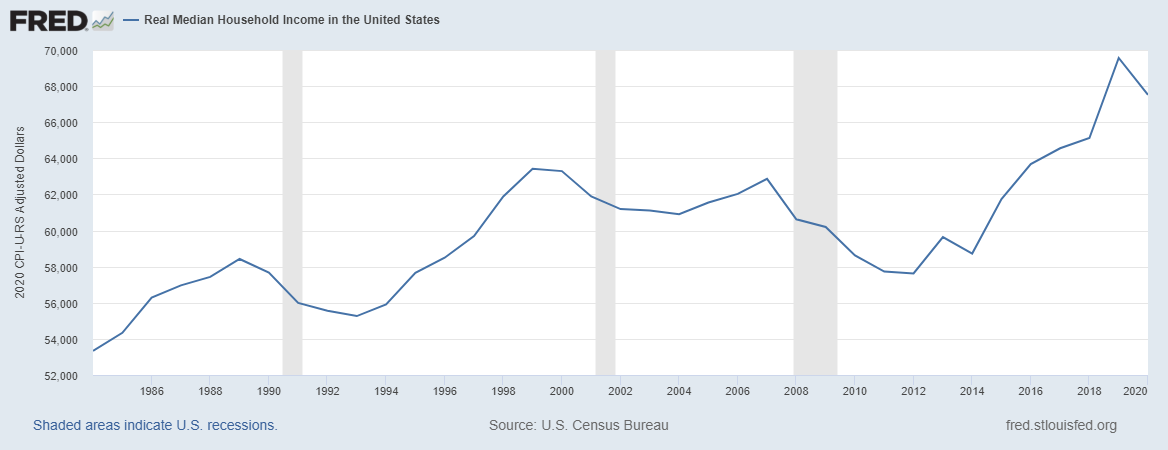

Our economic expansion never really took off, to begin with. The wealth that many baby boomers accumulated, for instance, was in the real estate and stock markets - markets that are not contributory to tangible wealth nor wealth accumulation. A house or a strip mall or a tower is only worth, ultimately, what its use is to someone and how much they need it for their own transitory wealth accumulation. In the example of houses, at the mean, were $50,000, before mortgages became easier to get. By the 1990s, this had risen to ~$80,000, and now, is at a phenomenal $276,000. The issue, now, is if wealth has been accumulated to pay for these houses, which, it definitely has not to make any sense for such a heightened average price:

This very issue hinges on the fact that credit expansion is dismal at the level that would justify such high asset prices. The issue gets even worse, as I mention in The Coming Housing Crisis, the reason the only housing you see being constructed these days is “luxury” apartments because the guys who build them know they won’t get their money if they build anything else. They need a bunch of units at high prices, or it just isn’t worth building. Now, if you are keen enough, you might understand what an existential issue that is - the price to play is too high, and even then, it’s not even worth it because the market is so elevated, and based on the past, has to drain excess debt from its piping.

So we are beginning to understand that the issue is not just a debt issue, but where that debt has been allocated (and that’s just within the American economy). Based on my theory, this debt easily expanded due to the great global GDP growth, regardless of even our own, that allowed for our economy of consumption to grow throughout the latter half of the 20th century. Unfortunately, this has reached a tipping point, as the rest of the world since 2008 has experienced pitiful growth due to their own dollar-denominated debt problems.

Based on my theory, as well, this means the debt will have to be drained from the system, and then the mechanisms for credit expansion will have to be hindered as well, so that we do not make the same mistake we did in 2008, where we thought we could keep issuing consumer debt, but we never got back to where we were, nor will we. This debt will have to be extinguished, and likely, there will be an event where the excess liquidity put into asset prices (especially housing real estate and stocks) will have to be converted into dollars to pay off all of this debt. This will cause a massive bid-down in the price of all assets, and we will finally be able to experience the level of credit contraction a healthy economy needs, before we can move on.

This is where we get to my own perspective and personal biased outlook - I do not think the credit contraction will be a few year, or couple decade long endeavor, however. It will have to last at least a lifetime as we experience a natural process of population decline, and extinguishing of infrastructure that is excess - physical, but also governmental and financial excess infrastructure. There is too much to maintain, and we must get rid of it, before it becomes a burden on future generations. The 21st century must be a century of reorganization and infrastructural decay, or we are doomed to a greater collapse within this century, or the next.

The unfortunate outcome of this event, of which I will call The Great Contraction, will not benefit anyone, but those of indigence and who are barely getting by, and those of net debtor status, will experience the brunt of this, and those are whom I pity most, because they were led astray by a system that gaslit them into thinking they were meant to be indebted servants. However, they will find peace in becoming more useful, resourceful, and skilled than their recent ancestors, and provide a better future for their children, because they are the ones that will have to understand what Hard Times are. If you aren’t ready for them, you doom future generations. Bless The Silent Generation for understanding their lot and doing what they had to do.

“The real tragedy of the poor is the poverty of their aspirations.”

Adam Smith

Jesus be with you all.