Central Banking: Explaining Monetary Madness

Central Banking: Explaining Monetary Madness

Just wanna thank Joseph Wang for his extremely important book, Central Banking 101. Beyond anything I’ve learned, that book has cleared up so much confusion I previously have had, and if you are looking for answers like I was, I think that’s a great book to start out with. Just thought it was appropriate to give credit where credit is due.

I think it is extremely important to demystify a few esoteric phenomena and terms that are integral to the banking system that most people hear, but do not understand. On my journey to understand why our monetary system is broken, I’d come across so many terms that were unhelpful and unintuitive, and wrong ideas that were intuitive but wrong.

We will obviously focus on the US and USD, not only because it’s what I deal with, but because it’s really the only currency that matters. For the uninitiated, I do not say that in some jingoistic sense. Far from it, I think the dollar being the “world reserve currency” is inherently stupid and has proven to lead to deflationary pressures on developed economies that have saddled themselves with debt, dooms developing and emerging economies to being thrown from the ship when there is a global economic slowdown, and has doomed current young and future generations to losing hope for any kind of risk-on sentiment that would give them a plethora of ample opportunity at becoming successful through hard work and ambition.

To begin, I’d like to talk about the basics of how money works in the modern economy and financial system. Starting first with the four kinds of money:

Paper Currency/Fiat Curency/Cash: This is the physical money you draw from an ATM, use to pay for things without being tracked, or to plain ole’ just show off. Cash is technically a liability of the US gov’t, but is not “insured” like Treasuries are. Ultimately, it is backed by said Treasuries (US gov’t debt), but ultimately is printed when there is demand for dollars to be put into ATMs, or for when a bank that doesn’t have an account with the Fed makes a deal with another. That’s where the armored trucks loaded with those beautiful green pieces of paper come in to play.

Central Bank Reserves: This is the money of the banking system. Central bank reserves (AKA, bank reserves) never leave the balance sheet of the Fed, and act as sort of "ledger system” for which the banking system can then make bank deposits from. This is where “fractional reserve banking” comes into play, where banks create bank deposits based on those central bank reserves.

Bank Deposits: This is the money you see in your bank account on your phone app or bank’s website. It is the money created by the bank, purely at their own discretion. If a bank makes too many bad loans, it will not be able to convert its bank deposits into cash as it must sell all of its assets for a lower and lower prices, and use the last of its assets to pay for its bad decisions. This leads to bank-runs, wherein customers who have bank accounts with said bad bank will not be able to convert their bank deposits to the equivalent amount in paper currency. So bank deposits can be made worthless. All you get for having them is FDIC insurance for $250,000 you have in your checking or savings accounts.

US Treasuries: This is the debt of the US government. It is issued to pay for the bills of the US government. It is essentially money that pays you interest for owning. Nowadays, it has become the real blood of the financial system as it is the only preferred collateral in the trades of the banking/financial system. This is why the Reverse Repo Facility has been so highly used, and is a sign of a crisis of confidence, as not only banks prefer to be in treasuries and repos rather than risking their money on the market, but the price to pay for other things in the financial economy only accepts treasuries as money.

So, imagine a bank has made a bunch of bad loans, it is forced to sell its assets, well customers will get antsy and start “pulling their money” out of the bank. What that really means is they will convert those bank deposits for cash. Well, the bank doesn’t have enough cash, and will ultimately be forced to the Discount Window at the Fed, wherein they will be able to get more bank reserves, but at a higher interest rate, and nowadays, that would be financial suicide as no other bank would be very eager to do business with them. This is what led to the fall of Lehman Brothers and Bear Sterns. They couldn’t get enough bank reserves to back their bank deposits. Their bank deposits, being made worth less, were made worthless as their customers took their money and ran. Their bad loans were specifically due to the fact they were making easy money by creating private-label Mortgage-Backed Securities which were seen as pristine collateral much as US Treasuries. This is essentially what the Great Financial Crisis was about, and why there is a giant issue with the monetary system that can only be solved with collapse.

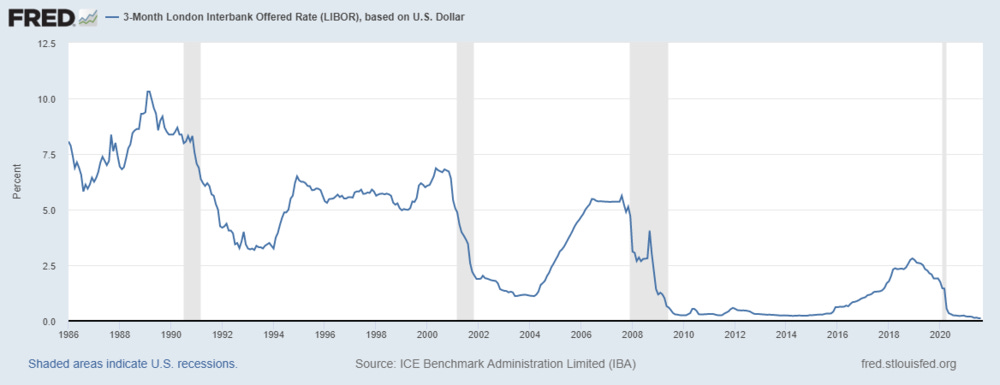

Moving on, we have the eurodollar and the Eurodollar System. Simply put, eurodollars are dollars outside the regulatory domain of the Fed. This also happens to be 55% of the entirety of dollars that exist. Dollars are created outside of the US all the time, as loaning in them by foreign central banks and commercial banks is continuously done. This leads to continuous dollar shortages/need for dollar funding, and a constant need for dollars. Ultimately, in the case of low growth and the brave new world of economic slowdown, most nations will need dollars to take care of the many bills and net deficits they have.

LIBOR, the London Interbank Offering Rate, is the agreed-upon rate that the eurodollar market uses to loan dollars. For decades, much like US Treasury rates, it has been going down. Why is that? Because demand for dollars continues to rise, as the growth continues to fall. Simply put, people want dollars (liquidity) and not things. Instead of investing or speculating, they want insurance and guaranteed risk-off income.

.png")

Primary Dealers: These guys are the pipeline from the Fed to everybody else. They act as an artificial demand for Treasuries, so technically there can never be no-bid on US Treasuries (technically). Primary Dealers, most prominently, act as the intermediary for entities that want treasuries, and therefore, repo. As per Joseph Wang’s example in his fantastic book Central Banking 101:

A Hedge Fund may want to take out a one-month loan from a (primary) dealer collateralized by some (treasury) securities. A (primary) dealer would make the one-month repo loan, then source the money by borrowing from one of its investors clients using those same securities as collateral. However, the dealer will likely borrow on an overnight basis instead of matching the maturity of the two loans. Since the interest rate for overnight loans is lower than the rate for one-month loans, the dealer will be able to earn the difference between in interest it receives from the one-month loan to the hedge fund and what it pays its investor client for an overnight loan.

What’s important to understand is that the lifeblood of the financial economy is built on faith, and there is little of that faith left, so the Fed tries to keep the lifeblood moving with drugs that are less and less potent the more and more they use them. The most common drug they’ve liked to use is the labyrinthine Quantitative Easing (QE). You hear from everyone about how bad, how inflationary, and how dangerous QE is. It’s not bad. In fact, it’s not even useful. It literally does nothing. What the hell is it though?

Quantitative Easing is literally just the Fed buying up Treasuries from banks, using central bank reserves (remember, the money used between banks.) Theoretically, this should encourage banks to lend, right? Because now there’s more liquidity, right? Ehem. WRONG! Banks don’t magically want to lend simply because now they have more of those special bank reserves. What makes them want to lend? Well, signals in the economy that there is a move towards growth. Henry Fords and Thomas Edison. They want to see less regulation and more risk-on. However, all they can see are extremely indebted manchildren, lowering birthrates, more government regulation, the entirety of the collateral market fail in 2008, GDP flatten in most countries for the last 13 years…. I could go on. They don’t want to lend. The signal for risk-on has to be made by the market. People have to be interested in producing, but debt simply doesn’t go to productivity like it once did. Instead it is largely consumer-based.

For a plethora of reasons, banks aren’t interested in lending, but ultimately, the number one reason is just faith that the system still has any luster left is really what scares them away from real risk. The crash of 2000 and 2008 really left the failures of loose money raw in the minds of Americans, and again, continues to be that way. Nowadays, the degenerate, failure powers-that-be are hopelessly searching for a new system as they are aware this Eurodollar/Dollar standard has been a failure and will lead to a defaulting domino effect escapade. It’s just a matter of when, and not if.

Before maybe 2019’s Repo Madness, the half a dozen QEs, Europe’s inability to induce growth via negative interest rates, the Japanese gov’t basically buying up its entire economy and still not being able to induce growth, and now the grand finale being the crash of 2020 and the horrible totalitarianism and societal mass hysteria that has followed seems to be the final nail in the coffin of this Eurodollar System… now it’s just a zombie waiting to have it’s brains blown out once and for all.

Some extremely important but more easily-explained away terms:

Security: Financial instruments that can be bought and sold.

Mortgage-Backed Securities (MBS): Securities that are backed by housing debt.

Agency MBS: MBSs that are backed by Fannie and Freddie Mac (the US gov’t).

Private-label MBS: The same security, but privately collateralized, so not gov’t-backed. This was partly responsible for the GFC. Yes, banks legit thought they could securitize this and it would be just as pristine as 100%-insured interest-paying US Treasuries. Also, yes, they’re still used, but nowhere near as much. Why? Because foreigners like to use them because they pay a higher interest rate. Domestically, our banks are too aware of low growth and the ensuing crisis to trust anything much other than Treasuries.

“With a gun, a man can rob a bank. With a bank, a man can rob the world.”

Carter Glass